Finance teams that have deployed robotic process automation (RPA) know what comes after the rollout. The tool handles routine volume cleanly, then creates a parallel manual process for everything it can't resolve. That second queue is usually where the costly exceptions accumulate. AI agents handle that queue differently, since they don't need a pre-written rule for every edge case; they reason about context and act.

TL;DR

- AI agents handle judgment-heavy finance workflows (fraud detection, reconciliation, compliance) without pre-written rules for every edge case.

- By 2028, 33% of enterprise software will include agentic AI, up from less than 1% in 2024.

- Finance ops teams are deploying agents on platforms like Pazi to own multi-step workflows end-to-end.

Table of Contents

- What AI agents do that RPA can't

- Five finance workflows where agents are in production today

- How to deploy an AI agent on your finance team

- Four metrics tell you whether your finance agents are working

What AI agents do that RPA can't

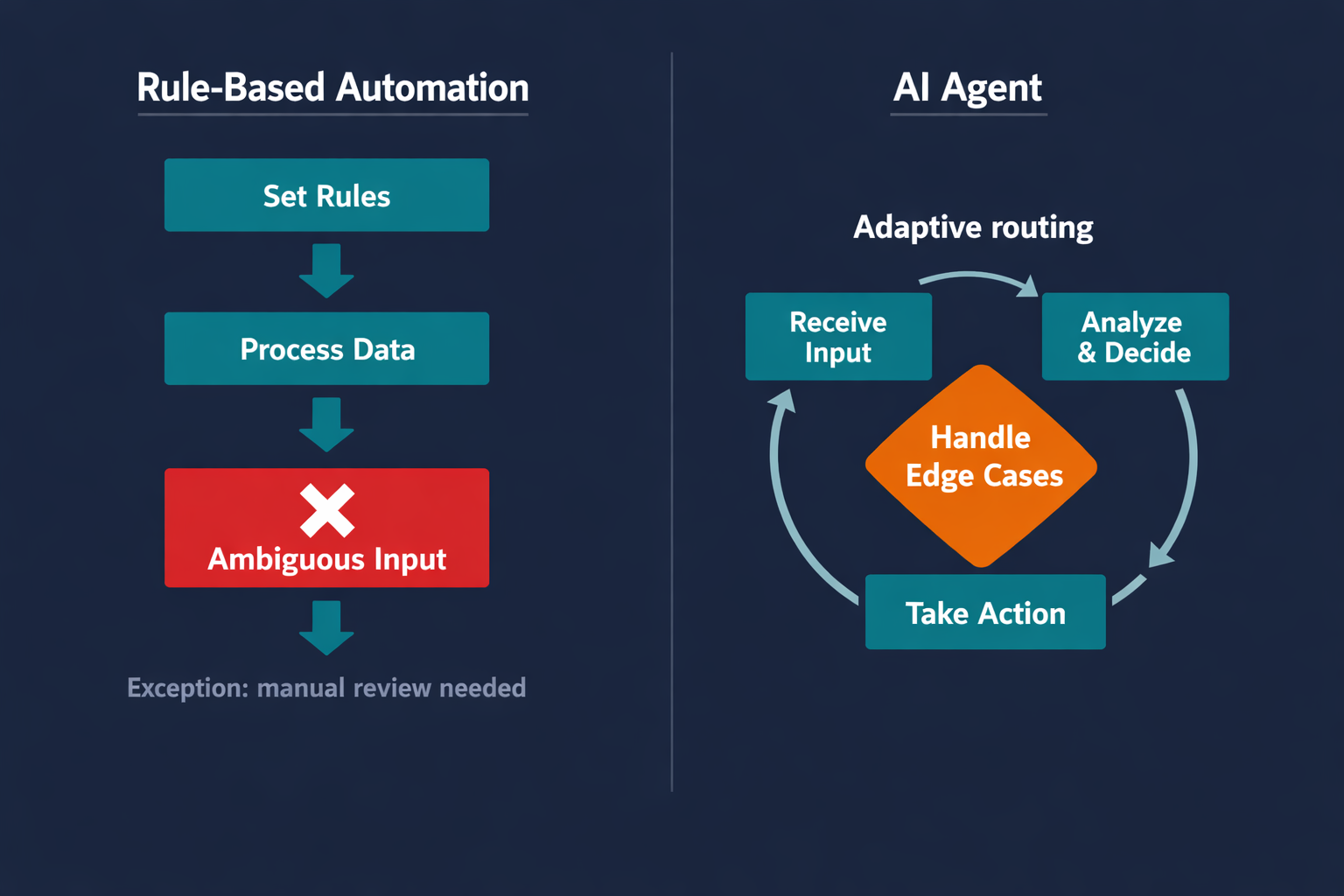

Rule-based systems are deterministic by design. Feed them a structured input and they produce a reliable output, which works well for the predictable portion of any finance workflow. Finance generates exception volume that outpaces any static rule set, since the inputs carry context that changes what the right action is, and no rule written in advance covers every version of that context.

Rules break on edge cases. Agents adapt.

Rule-based automation works when every input is clean and every path is pre-mapped, but finance workflows aren't built that way. Fraud patterns shift as fraudsters adapt to detection systems; regulatory requirements update without warning; and a reconciliation item that doesn't match may need resolution through one of several different paths depending on context that no static rule set captures cleanly, because the context itself changes with each instance.

RPA systems are engineered for predictability; give them a structured workflow and they perform it consistently at scale. Give them an exception and they stop, throw an error, or silently misroute the item to a queue that a human then works through manually. The automation was supposed to reduce that manual queue, but in practice it moves the queue downstream and adds a routing step on top.

Finance runs on exceptions; rules were never designed to handle them.

Understanding what makes an AI agent truly autonomous is the key to the difference, since agents don't follow a static decision tree but instead observe, reason, and act based on context. When a transaction doesn't match a known pattern, an agent reads the surrounding data, infers the most likely resolution, and either acts on it or escalates with a clear explanation of why. The exception queue shrinks because the agent handles a significant portion of what was previously routed there by default.

What the agent layer adds to a finance workflow

The practical difference shows up most clearly in fraud detection, reconciliation, and compliance monitoring, the three workflow types where finance teams spend the most time. RPA can move data between systems. Agents can assess whether the data is correct, determine what the right action is given the full context, and close the exception without waiting for a human to review the item first.

The architecture shift is from automation that requires clean inputs to automation that can reason about messy ones. Finance data is almost always messy. Transactions arrive with missing fields, reference numbers that don't match across systems, and contextual signals that only matter if you can read them alongside the transaction itself. Agents can handle that; static workflows can't.

| Workflow | RPA approach | AI agent approach |

|---|---|---|

| Fraud detection | Rule thresholds: flag if transaction exceeds a set amount or occurs in a flagged location | Behavioral pattern matching: flag if transaction deviates from the account's normal context, even at normal amounts |

| Reconciliation | Match rows by reference number; route unmatched items to exception queue | Match by reference, amount, and contextual signals; auto-resolve likely matches; escalate genuine ambiguity only |

| Compliance monitoring | Scheduled rule checks against a known regulation list | Continuous feed monitoring; flags new requirements and maps them to affected positions in near real-time |

The difference between RPA and an AI agent isn't processing speed or throughput. It's that an agent can handle a transaction it has never seen before. Finance teams deal with novel situations every single day, and RPA was never designed for that.

Five finance workflows where AI agents are in production today

Agents are running across fraud detection, reconciliation, compliance, FP&A, and autonomous payments in production today, not as pilots. These aren't demos.

Fraud detection

Stripe Radar evaluates each transaction using behavioral pattern matching rather than static thresholds. The agent assesses the transaction against the account's historical context, device fingerprint, network signals, and transaction velocity before the payment clears. Featurespace takes a similar approach with its ARIC risk hub, building an individual behavioral baseline for each account and flagging deviations that rules-based systems would miss entirely because the deviations happen within normal dollar amounts.

The persistent failure mode in rule-based fraud systems is high false positive rates. A rule that flags all international transactions above a set threshold catches fraud and also catches every legitimate business traveler in the review queue. Agents tune dynamically based on what is normal for that specific account, which brings false positives down without increasing fraud exposure. The reduction in false positive volume also frees fraud review teams to focus on genuine alerts rather than clearing a backlog of legitimate transactions that tripped a static rule.

Reconciliation and the month-end close

BlackLine, Workday Financial Management, and NetSuite have all developed agent-assisted reconciliation flows that go beyond row matching. The agent owns the full reconciliation cycle, matching items, auto-resolving high-confidence matches, surfacing a prioritized exception queue, and generating the sign-off documentation for the finance controller. Teams close faster because the agent handles the volume; humans review the genuinely ambiguous items rather than every line in the ledger.

SAP Concur deployed an agentic "Receipt Analysis Agent" built on Google Cloud's Gemini models that demonstrates what end-to-end ownership looks like for expense reporting. Rather than scanning receipts and stopping there, the agent reasons about missing context by pulling trip itinerary data to infer vendor location and complete expense entries without manual intervention. The reasoning step that previously required a human to look up external context is now handled by the agent before the expense item reaches a reviewer at all.

Compliance monitoring

Compliance officers at financial institutions track regulatory feeds from the SEC, FCA, FINRA, and local equivalents in parallel. Bloomberg Terminal provides the data layer; ComplyAdvantage handles screening and sanctions monitoring. The agent watches those feeds continuously, flags new or updated requirements, maps them to affected positions, and drafts the initial compliance memo for officer review and sign-off.

The gap that closes is timing. Regulatory changes don't align with quarterly review schedules, and a compliance team working manually will always lag by days or weeks. An agent running a continuous monitoring loop surfaces an update within hours and routes it to the right person before the change takes effect. The compliance officer stops being the person who discovers the change and becomes the person who decides what to do about it.

FP&A and forecasting

FP&A analysts at most mid-market companies spend more time aggregating data than analyzing it, and Anaplan, Pigment, and Workday Adaptive have all built agent-assisted workflows that restructure this ratio. The agent pulls actuals from the ERP, compares them against the budget model, flags variances above the defined threshold, and generates a variance narrative for the CFO dashboard. The analyst reviews the narrative, adds judgment where context matters, and applies the remainder of their time to analysis rather than data wrangling across three systems that never quite align.

The outcome isn't just faster reporting. It's that the analyst is thinking about what the numbers mean rather than why three source systems have different values for the same line item.

Autonomous payments

PayPal and Google Cloud announced an agentic commerce solution for merchants built on Agent-to-Agent (A2A) Protocol and Agent Payments Protocol (AP2). The PayPal agent communicates with the merchant's agent over the open A2A Protocol, and the AP2 layer handles trust, accountability, and fraud controls for settlement. Agents negotiate and complete payments autonomously, without a human approving each transaction. This is the clearest 2026 signal that AI agents in finance have moved from workflow support to financial execution.

"The bottleneck in finance automation isn't finding workflows to automate. It's building agents that can handle the 20% of transactions where context changes the answer every time. That's where the month-end close gets held up. That's where the fraud slips through. That's where FP&A misses the variance that mattered. Agents that can read context are the ones that actually close those gaps."

How to deploy an AI agent on your finance team

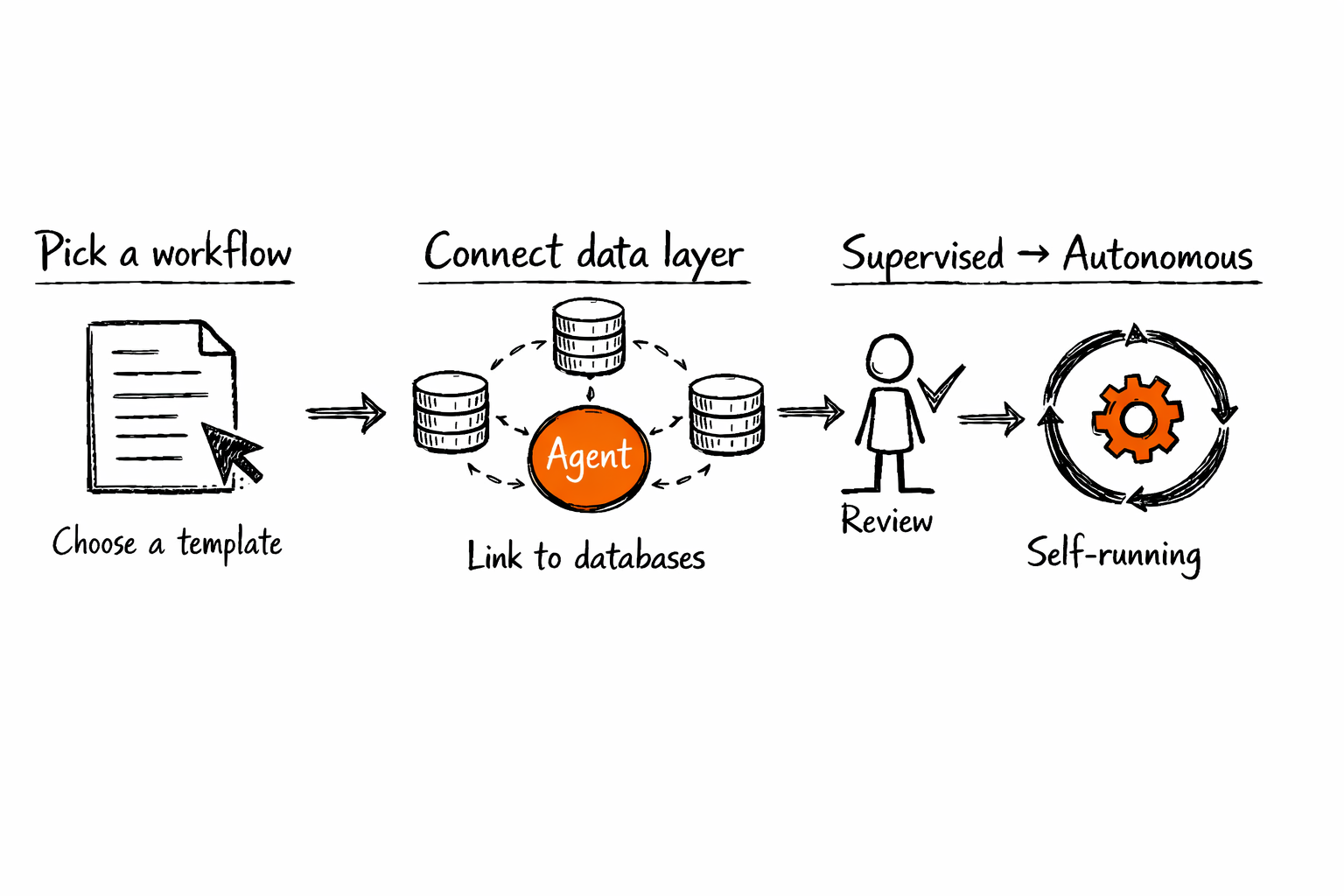

Most teams get stuck choosing the wrong first workflow. The right entry point has clear inputs, defined success criteria, and enough transaction volume to make the agent's accuracy measurable within the first two weeks.

Phase 1: Pick one workflow with clear inputs and outputs

Don't start with FP&A. The outputs of an FP&A workflow require executive context that a new agent can't reliably infer in its first weeks. The failure mode is a variance narrative that reads as authoritative but misses the business context your CFO will flag in the first review meeting, which erodes confidence before the agent has had time to prove itself.

Start with reconciliation or fraud flagging, since both are bounded, high-volume, and measurable enough to show clear results within the first two weeks. Before any agent configuration happens, write down what "correct" looks like. For reconciliation, that means specifying what constitutes a clean match, what gets escalated, and who owns the exception queue. For fraud flagging, write down the acceptable false positive rate and what happens to a flagged transaction while it's under review. If you can answer both questions in two sentences each, the workflow is ready for an agent. If you can't, the workflow definition needs to happen before the tooling does.

Starting narrow also gives the agent a clean data set to calibrate against. An agent learning on a tightly scoped, well-defined workflow reaches useful accuracy faster than one dropped into a sprawling process with ambiguous success criteria.

Phase 2: Connect to your data layer

Integration is the actual deployment work, not the agent configuration. The agent needs access to the transaction data source, the GL or ERP system, and an output channel for routing results (Slack, a shared finance dashboard, or direct email to the exception queue owner). Most finance systems support read-only API access, and webhook-based output configuration is straightforward. The real work is mapping what data the agent needs, where it lives, and what format it arrives in.

The integration layer determines how quickly the agent reaches useful throughput, and the complexity grows in proportion to the number of systems in scope. Teams running operations workflow automation across multiple data sources find this is where most of the deployment effort lives. Platforms like Pazi handle this integration layer directly. The agent lives where your finance team already works, connects to the data it needs, and routes outputs to the right people without custom engineering on every connection point.

Phase 3: Run supervised first, then autonomous

Weeks 1 and 2, a human reviews every agent action before it fires, since the goal isn't to check the agent's work at scale. It's to identify where the agent's judgment is reliable and where it needs more explicit escalation criteria before being trusted to act autonomously.

In weeks 3 and 4, the human reviews only flagged exceptions while the agent runs independently on clear-match items and escalates genuine ambiguity. This phase surfaces the specific edge cases that need explicit rules rather than contextual inference, and identifying those cases early prevents false confidence in the agent's coverage.

From week 5 onwards, the agent runs autonomously with defined escalation rules and a configured exception routing path. When you have two or more agents running in parallel, you're building toward multi-agent systems where agents hand off between each other automatically. A fraud flag from the fraud agent triggers a compliance review from the compliance agent without a human routing the handoff. The finance ops layer starts to run itself on the workflows where the inputs and outputs are well-defined.

If you can't describe what "correct" looks like in 30 seconds, the workflow isn't ready for an agent.

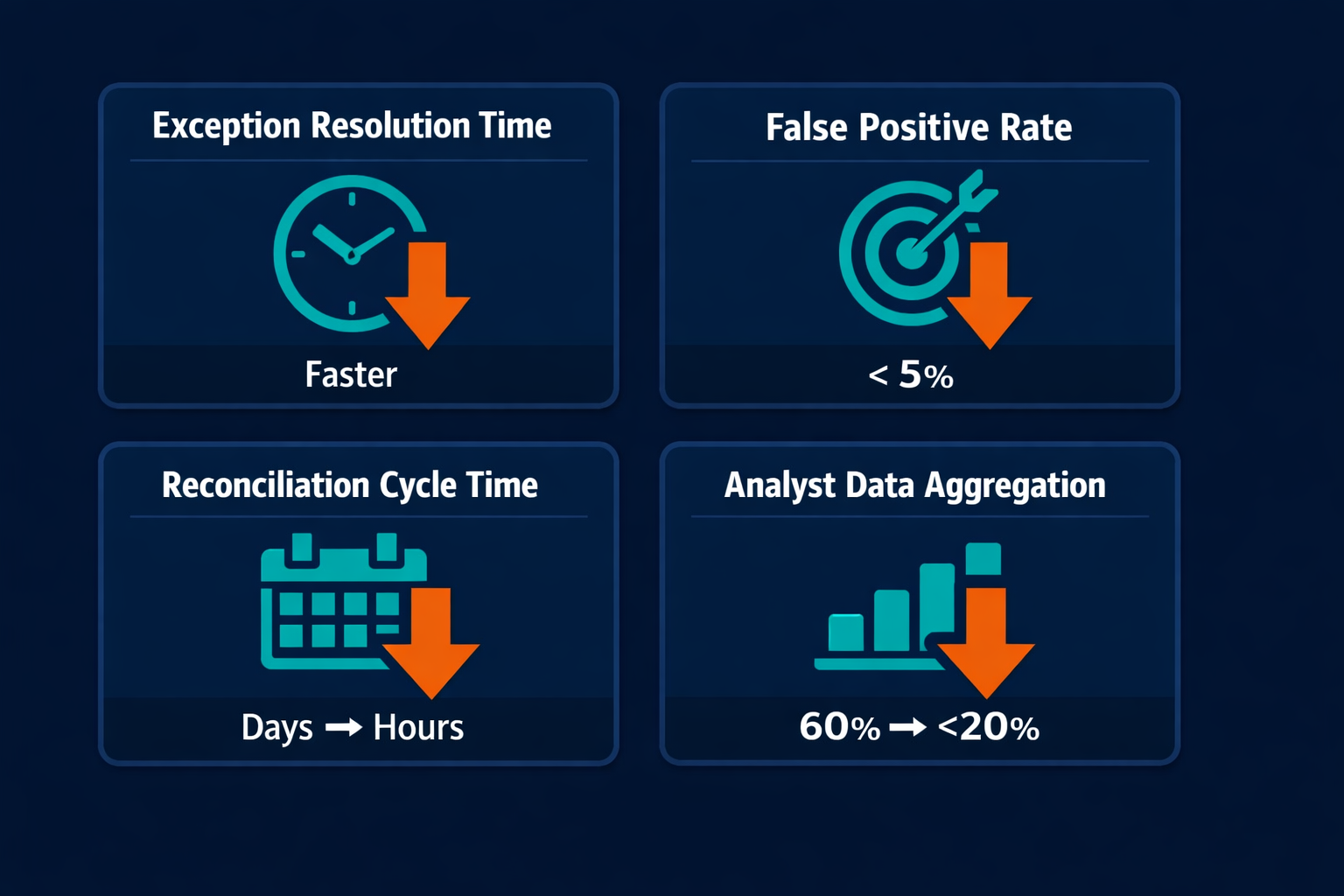

Four metrics tell you whether your finance agents are working

Four metrics tell the full story on whether a finance agent is doing its job. If all four are moving in the right direction after the first 30 days, the agent is working.

The four metrics that matter

| Metric | What it measures | Target direction |

|---|---|---|

| Exception resolution time | Speed to close a flagged item | Down vs. manual baseline |

| False positive rate | Fraud/compliance flags that weren't real issues | Down to under 5% |

| Reconciliation cycle time | Time from period close to reconciled GL | Down from days to hours |

| Analyst data aggregation time | Percentage of FP&A time on pulling vs. analyzing | Down from 60-70% to under 20% |

The adoption curve confirms that these metrics are becoming standard operating benchmarks across finance teams. IBM Think, citing Gartner, projects that by 2028, 33% of enterprise software applications will include agentic AI, up from less than 1% in 2024. Finance is a lead adoption sector because the ROI on reducing exception resolution time and analyst aggregation time shows up directly on the cost structure. It doesn't require an attribution model to justify.

What good looks like in year one

Finance teams running agents in production for 12 months consistently report the same three outcomes, regardless of which workflow they started with. Reconciliation cycle time drops from two to three days to two to four hours; FP&A analysts shift from data aggregation toward analysis and narrative work; and false positive rates in fraud and compliance monitoring decrease as the agent's behavioral baselines grow more accurate with transaction volume, because the agent is calibrating against a richer picture of what normal looks like for that specific portfolio.

The metric that matters most in year one isn't the efficiency gain; it's the exception escalation quality. An agent that escalates the right items and handles the rest cleanly is working correctly. An agent with a climbing exception rate is working around gaps in its data access, not around genuine transaction ambiguity. The escalation rate is a diagnostic, not just a performance number.

If the exception rate climbs after deployment, the agent has bad data access; fix the integration, not the agent.

The longer-run benefit compounds because the agent's accuracy improves with volume. A reconciliation agent that starts with solid coverage in month one will reach higher accuracy by month six as it builds a richer contextual model of the portfolio it's working with. The baseline shifts upward over time. That compounding effect is why finance teams that deploy agents earlier gain a structural advantage over teams that wait for perfect conditions before starting.

The ROI on finance agents isn't a one-time gain. It accumulates as the agent's accuracy improves with volume and as the team stops designing workflows around the assumption that humans will be in every loop. The teams that see the biggest returns aren't the ones with the most sophisticated agent configurations. They're the ones that gave the agent a well-scoped workflow, clean data access, and time to calibrate.

Pazi is a platform built for finance operations teams that need agents to do real work, not generate reports. For finance teams, that means agents running reconciliation, fraud monitoring, and compliance workflows from the same workspace where the team already operates, with outputs routed automatically to the right people without manual hand-offs at every step. If you're ready to move your first finance workflow from manual to agent-owned, start here.